Создание вашего первого атомного арбитража в…

**Краткий ответ**. Атомарный арбитраж – это одна транзакция, в ходе которой актив покупается дешево в пуле А, продается подороже в пуле Б и полностью возвращается, если сделка туда

Краткий ответ. Атомарный арбитраж – это одна транзакция, в ходе которой актив покупается дешево в пуле А, продается подороже в пуле Б и полностью возвращается, если сделка туда и обратно невыгодна. В 2026 году проще всего начать с арбитража ETH/USDC между двумя пулами на Base или Arbitrum — одна и та же пара активов, разные DEX (Uniswap V3 против Aerodrome/SushiSwap), небольшой дрейф цен после большого свопа в одном пуле. В этой статье мы разберем это: математику пула, структуру calldata, проскальзывание, симуляцию и то, как на самом деле должно выглядеть ваше первое успешное исполнение.

Если вы еще не знаете, Что такое MEV, начните с этого.

Что делает арбитраж «атомарным»

Три свойства:

- Единая транзакция. Покупка и продажа происходят в одной и той же транзакции, а не в двух последовательных.

- Условное исполнение.

require(profit > 0, ...)откатывает транзакцию, если прибыль не материализуется. - Флэш-заём. Капитал можно взять в долг и вернуть в рамках одной транзакции.

Именно атомарность защищает вас от риска исполнения. Если что-то пойдет не так в середине транзакции, всё откатывается, и вы платите только за газ, а не теряете основную сумму.

Теория за 60 секунд

Два пула оценивают один и тот же актив немного по-разному. После того, как крупный своп по пулу А отталкивает его цену от рыночной, пул Б становится дешевле. Вы покупаете на B, продаете на A, фиксируете спред.

Для двух пулов AMM, использующих постоянный продукт (x * y = k):

Effective_price_A = (reserve_y_A / reserve_x_A) × (1 - fee_A)

Effective_price_B = (reserve_y_B / reserve_x_B) × (1 - fee_B)

Если Effective_price_A > Effective_price_B + slippage_buffer, арбитраж существует.

Оптимальный размер сделки — это размер, который уравнивает предельные цены двух пулов. Существует решение в закрытой форме, но вы можете использовать двоичный поиск или позаимствовать помощников Foundry.

Выбор первой пары

Выбирайте пару с:

- Высокий объем в обоих пулах. Низкий объем = устаревшие цены, но нет глубины заполнения.

- Один и тот же уровень комиссионных в обоих пулах (например, Uniswap V3 со скоростью 5 б.п. или Aerodrome 5 б.п.). Разные уровни комиссий усложняют математику.

- Прямая пара, а не многопереходная. Сохраните многопереходную настройку на будущее.

- Ликвидный базовый актив. ETH/USDC, ETH/USDT, USDC/USDT. Не экзотика.

Рекомендуемая стартовая пара на Base: WETH/USDC. Два пула для сравнения:

- Стейбл-пул Aerodrome (комиссия 1 б.п.)

- Пул Uniswap V3 с уровнем 0,05% (комиссия 5 б.п.)

У них сотни миллионов TVL и предсказуемое поведение спреда.

Инструменты

Вам нужно:

- WSS-эндпоинт для вашей целевой сети (например, WSS для Base через Alchemy или собственный узел).

- Foundry, установленный локально для симуляции.

- Тестовый кошелек, пополненный на $50–100 в ETH на газ и оборотный капитал.

- ABI для контрактов маршрутизаторов обоих DEX.

Вся эта настройка выполняется на ноутбуке. Мы еще не в продакшене.

Шаг 1: Следите за спредом

Подпишитесь на свопы в обоих пулах и вычисляйте спред для каждого блока:

js

const aero = new ethers.Contract(AERO_POOL, AERO_ABI, provider);

const uni = new ethers.Contract(UNI_POOL, UNI_ABI, provider);

provider.on('block', async (n) => {

const [r0a, r1a] = await aero.getReserves();

const [r0u, r1u] = await uni.getReserves();

// ... compute price each side, then spread

});

Наблюдайте в течение часа. Большинство блоков: спред <1 б.п. Некоторые блоки (после крупных свопов): спред 5–30 б.п. Отметьте частоту появления прибыльных спредов.

Шаг 2: Порог прибыльности

Точно определите, что значит «прибыльно». Для рабочего объема в $5000:

gross_profit = trade_size × spread_bps / 10000

gas_cost = gas_units × gas_price (в USD)

slippage = trade_size × ваш_буфер_проскальзывания

fees_paid = trade_size × (fee_A + fee_B)

net_profit = gross_profit − gas_cost − slippage − fees_paid

На Base газ для транзакции арбитража между двумя пулами составляет ~250–400 тыс. газовых единиц. При типичной для 2026 года цене газа ~0.001 gwei это $0.04–$0.10. Дешево.

Для сделки на $5000 со спредом 8 б.п.:

- Брутто: $4.00

- Газ: $0.08

- Буфер проскальзывания: $1.50 (3 б.п.)

- Комиссии: $3.00 (уже учтены через проскальзывание в пуле)

- Чистая прибыль: ~$2.40

Это тонкая маржа. Используйте спред > 10 б.п. как минимальный порог фильтрации для сделки на $5 тыс.

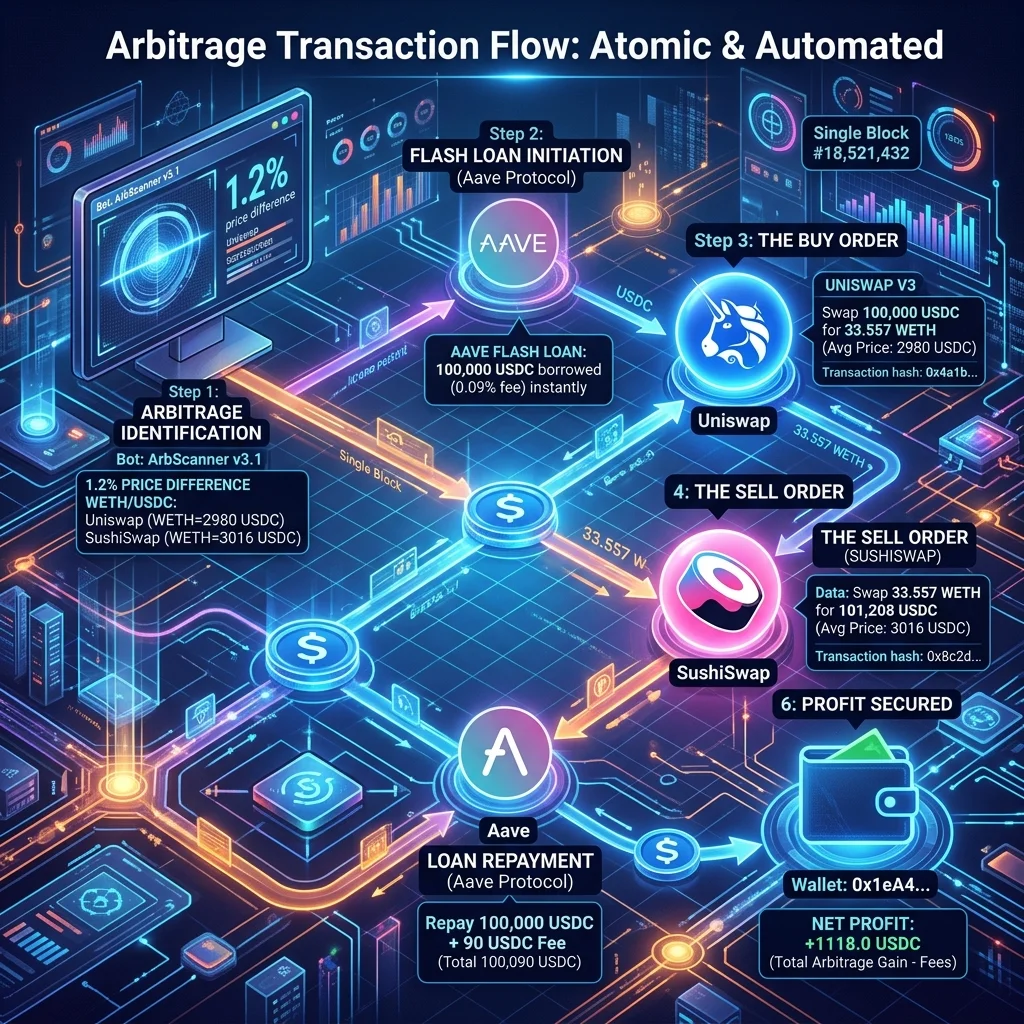

Шаг 3: Формирование calldata

Структура calldata для арбитража между двумя пулами:

1. Approve router_B (if not pre-approved) - skip in production with infinite approvals

2. swap on router_B: USDC → WETH

3. swap on router_A: WETH → USDC

4. require(usdc_out > usdc_in + min_profit, "unprofitable")

Для простоты используйте диспетчерский контракт, который выполняет все четыре операции за один вызов. FRB Agent поставляется с таким контрактом (верифицированным в каждой сети), либо напишите свой собственный минимальный контракт.

Минимальный пример на Solidity:

function executeArb(

bytes calldata buyCalldata,

bytes calldata sellCalldata,

address tokenOut,

uint256 minProfit

) external {

uint256 startBalance = IERC20(tokenOut).balanceOf(address(this));

(bool ok1, ) = router_B.call(buyCalldata);

require(ok1, "buy failed");

(bool ok2, ) = router_A.call(sellCalldata);

require(ok2, "sell failed");

uint256 endBalance = IERC20(tokenOut).balanceOf(address(this));

require(endBalance >= startBalance + minProfit, "no profit");

}

Реальные реализации сложнее (обработка собственного ETH, нескольких маршрутизаторов, обратных вызовов для пулов V3). Относитесь к вышеизложенному как к иллюстративному.

Шаг 4: Имитируйте каждую попытку

Перед отправкой смоделируйте передачу в разветвленной цепочке:

anvil --fork-url $RPC_URL --fork-block-number latest

cast send --private-key $TEST_KEY $DISPATCHER \

"executeArb(bytes,bytes,address,uint256)" \

$BUY_CALLDATA $SELL_CALLDATA $WETH 1000000

Если симуляция прошла успешно с прибылью > min_profit, можно отправлять транзакцию. Пропуск симуляции — причина №1 ревертов у начинающих ботов.

Шаг 5: Отправьте

Для Base отправьте данные в общедоступный мемпул (PBS в 2026 году пока не используется для большинства L2). Используйте умеренную плату за приоритет, чтобы попасть в следующий блок:

js

const tx = await wallet.sendTransaction({

to: DISPATCHER,

data: dispatchCalldata,

gasLimit: 500000,

maxFeePerGas: ethers.parseUnits('0.0015', 'gwei'),

maxPriorityFeePerGas: ethers.parseUnits('0.0005', 'gwei')

});

const receipt = await tx.wait();

console.log('Status:', receipt.status, 'Gas used:', receipt.gasUsed);

Если receipt.status === 1, вы его получили. Посмотрите receipt.logs, чтобы узнать фактическую полученную прибыль.

Шаг 6: Измерьте, что произошло

Ваши первые 20 попыток в основном будут:

- Реверт (опередил другой арбитражёр): 50–70%

- Исполнится, но хуже, чем в симуляции: 15–25 %

- Исполнится с прибылью: 10–25%

Это нормально. Соотношение улучшается по мере настройки (меньшая задержка, лучшая фильтрация сигнала, более разумный размер).

Что регистрировать:

- Спред на момент принятия решения

- Спред на момент исполнения

- Прогнозируемая прибыль против фактически полученной

- Использованный газ по сравнению с расчетным

- Почему произошел каждый реверт (помогают трейсы Foundry)

Шаг 7: Дорабатываем цикл

После 100 попыток вы увидите закономерности:

- Спреды выше определенного порога исполняются более надежно

- В определенные часы частота арбитражных возможностей выше

- Конкретные конкуренты быстрее вас в определенные периоды

Используйте эти закономерности, чтобы фильтровать, что вы отправляете. Меньше попыток, но более высокого качества — лучше, чем стрелять во все стороны.

Распространенные ошибки первого бота

- Отсутствует approval: контракт реверится при первом же вызове. Добавьте бесконечный approval в скрипт деплоя.

- Неправильный уровень комиссии пула: математика обещает прибыль, а реальный своп показывает убыток, потому что в расчетах использовался пул с комиссией 5 б.п., а вызывался пул с комиссией 30 б.п.

- Устаревшие резервы: вы прочитали резервы в блоке N, отправили транзакцию в блоке N+1 — состояние успело измениться. Перечитывайте резервы внутри контракта или используйте цены на основе callback.

- Слишком узкий лимит проскальзывания: сделки, которые были бы немного прибыльными, реверятся. Откалибруйте лимит по фактическим результатам в сравнении с симуляцией.

- Десятичные знаки токенов: у USDC — 6, у WETH — 18. Ошибка в расчетах на 12 порядков — распространенная ошибка.

Что дальше после арбитража между двумя пулами

Когда арбитраж между двумя пулами работает без сбоев:

- Треугольный арбитраж между тремя пулами: USDC → WETH → DAI → USDC.

- Мульти-DEX с поиском пути: динамически выбирайте, какие два из N пулов использовать.

- JIT-ликвидность: предоставление и вывод LP-позиции вокруг входящего свопа.

- Межсетевой арбитраж: требует моделирования стоимости моста (продвинутый уровень).

Стек навыков накапливается: математика пула → calldata → симуляция → задержка → биддинг. Атомарный арбитраж между двумя пулами — это основа.

Часто задаваемые вопросы

Нужно ли мне самому писать смарт-контракт?

Для обучения — да. Для продакшена FRB Agent поставляется с верифицированными диспетчерскими контрактами для каждой поддерживаемой сети. Используйте встроенные варианты в продакшене; пишите свой собственный для разработки, чтобы понять, как это работает.

Почему большинство попыток нерентабельны?

Вы конкурируете с ботами, у которых меньшая задержка, лучшая фильтрация сигналов и предварительно одобренная ликвидность. Новички получают оставшиеся спреды. Ничего страшного — есть остатки, которые стоит поймать.

С каким капиталом мне следует начать заниматься арбитражем?

$2–5 тыс. Ниже этого порога соотношение газа к капиталу слишком невыгодное. Выше этого порога можно масштабироваться после настройки.

Это разновидность сэндвич-атаки?

Нет. Арбитраж между двумя пулами на разных DEX не извлекает выгоду из чужого свопа — он уравнивает цены между пулами. Это полезно для протокола, а не вредно.

Могу ли я вместо этого запустить это на Ethereum L1?

Технически да, экономически болезненно для новичка. Газ L1 в размере 10–50 долларов за попытку съедает большую часть спредов при размере сделки <50 тысяч долларов. Начните с L2.

Связанное чтение

- Продвинутые стратегии арбитража ETH

- Фильтры и задержка сканирования мемпула

- Бэкран против сэндвич-стратегии

- Как протестировать стратегию MEV

- Руководство по крипто-арбитражному боту

Это инженерное руководство. Размещайте капитал только после запуска в тестовой сети или в режиме бумажной торговли. Не финансовый совет.

Похожие статьи

Дальнейшее чтение и инструменты

Обсуждение

Примечаний пока нет. Добавьте первое наблюдение или поделитесь ссылкой со своей командой на X (@MCFRB).