2026 年建立您的第一个原子套利:首次填充的理论

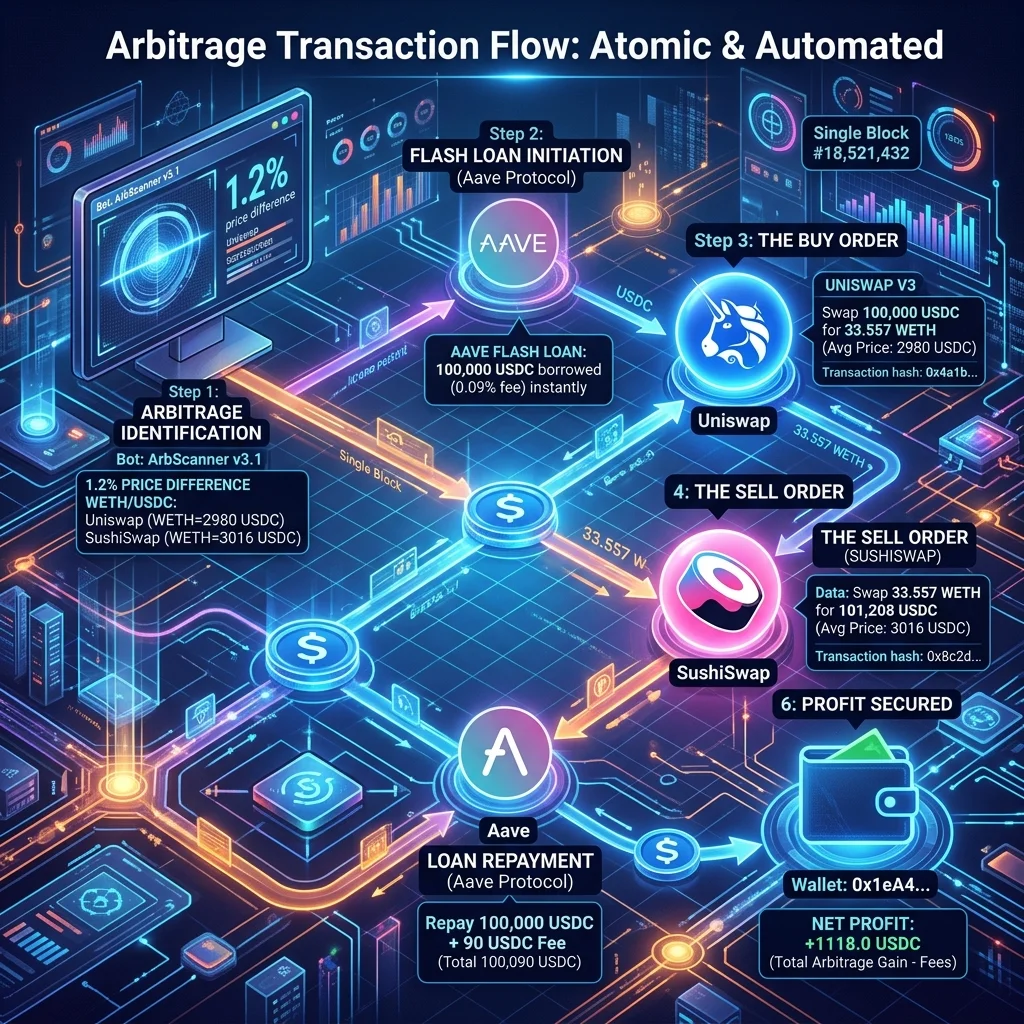

**简短回答** — 原子套利是一项单笔交易,在 A 池中以便宜的价格购买资产,在 B 池中以高价出售资产,如果往返无利可图,则完全恢复。 2026 年,最容易构建的第一个是 Base 或 Arbitrum 上的双池 ETH/USDC 套利 — 相同的资产对,不同的 DEX(Uniswap V3 与 Aerodrome / SushiSwap),在一个池上进

简短回答 — 原子套利是一项单笔交易,在 A 池中以便宜的价格购买资产,在 B 池中以高价出售资产,如果往返无利可图,则完全恢复。 2026 年,最容易构建的第一个是 Base 或 Arbitrum 上的双池 ETH/USDC 套利 — 相同的资产对,不同的 DEX(Uniswap V3 与 Aerodrome / SushiSwap),在一个池上进行大量掉期后价格漂移较小。本文将介绍它:池数学、调用数据、滑点、模拟,以及您的第一个实时填充实际上应该是什么样子。

如果您还不知道什么是 MEV,请从这里开始。

是什么让套利变得“原子”

三个属性:

- 单笔交易。 买入和卖出在同一个交易中,而不是两个连续的交易。

- 有条件执行。 如果利润未实现,则

require(profit > 0, ...)恢复。 - 可快速借用。 资金可以在交易内借入和偿还。

原子性可以保护您免受执行风险。如果在交易过程中出现任何问题,整个事情都会恢复,您只需支付Gas 费,而不是本金。

60 秒理论

两个池对同一资产的定价略有不同。在 A 池进行大量掉期后,其价格远离市场,B 池更便宜。您在 B 上买入,在 A 上卖出,获取价差。

对于使用常量积 (x * y = k) 的两个 AMM 池:

Effective_price_A = (reserve_y_A / reserve_x_A) × (1 - fee_A)

Effective_price_B = (reserve_y_B / reserve_x_B) × (1 - fee_B)

如果 Effective_price_A > Effective_price_B + slippage_buffer,则存在套利。

最佳交易规模是使两个池的边际价格相等的规模。有一个封闭式的解决方案,但您可以使用二分搜索或借用 Foundry 的助手。

选择你的第一双

选择一对:

- 两个池的交易量都很高。 交易量低=价格陈旧,但没有填充深度。

- 两个池的费用等级相同(例如 5bps Uniswap V3 与 5bps Aerodrome)。不同的费用等级使数学变得复杂。

- 直接配对,而非多跳。 保存多跳供以后使用。

- 流动基础资产。 ETH/USDC、ETH/USDT、USDC/USDT。不具有异国情调。

在 Base 上推荐的入门交易对:WETH/USDC。可比较以下两个池:

- Aerodrome 稳定币池(费用 1bps)

- Uniswap V3 0.05% 等级(费用 5bps)

它们拥有数亿的 TVL 和可预测的传播行为。

工具

您需要:

- 目标链的 WSS 端点(例如通过 Alchemy 提供或自托管的 Base WSS)。 2.本地安装 Foundry 进行模拟。

- 一个测试钱包,资金为 50-100 美元的 ETH,用于Gas + 营运资金。

- 两个 DEX 路由器合约的 ABI。

整个设置在笔记本电脑上运行。我们还没有投入生产。

第 1 步:观察价差

订阅两个池上的交换并计算每个块上的价差:

js

const aero = new ethers.Contract(AERO_POOL, AERO_ABI, provider);

const uni = new ethers.Contract(UNI_POOL, UNI_ABI, provider);

provider.on('block', async (n) => {

const [r0a, r1a] = await aero.getReserves();

const [r0u, r1u] = await uni.getReserves();

// ... compute price each side, then spread

});

观察一个小时。大多数区块的价差都 <1 个基点。部分区块(在大额交换之后):价差为 5–30 个基点。请留意有利可图价差出现的频率。

第 2 步:盈利门槛

精确定义“有利可图”。以 5,000 美元的操作规模为例:

gross_profit = trade_size × spread_bps / 10000

gas_cost = gas_units × gas_price(以美元计)

slippage = trade_size × your_slippage_buffer

fees_paid = trade_size × (fee_A + fee_B)

net_profit = gross_profit − gas_cost − slippage − fees_paid

在 Base 上,一笔双池套利交易的 Gas 用量约为 25 万–40 万个单位。按 2026 年约 0.001 gwei 的典型 Gas 价格计算,成本约为 0.04–0.10 美元,非常便宜。

对于价差为 8 个基点的 5,000 美元交易:

- 毛利:4.00 美元

- Gas:0.08 美元

- 滑点缓冲:1.50 美元(3 个基点)

- 手续费:3.00 美元(已通过池滑点支付)

- 净利润:约 2.40 美元

这是一个微薄的利润空间。将 5,000 美元交易的最低筛选门槛设为价差 > 10 个基点。

第三步:构建 Calldata

二池套利调用数据结构:

1. Approve router_B (if not pre-approved) - skip in production with infinite approvals

2. swap on router_B: USDC → WETH

3. swap on router_A: WETH → USDC

4. require(usdc_out > usdc_in + min_profit, "unprofitable")

为简单起见,请使用一个调度程序合约,在一次调用中完成所有四个操作。 FRB 代理发货一个(在每个链上验证),或者编写您自己的最小合同。

最小坚固性:

function executeArb(

bytes calldata buyCalldata,

bytes calldata sellCalldata,

address tokenOut,

uint256 minProfit

) external {

uint256 startBalance = IERC20(tokenOut).balanceOf(address(this));

(bool ok1, ) = router_B.call(buyCalldata);

require(ok1, "buy failed");

(bool ok2, ) = router_A.call(sellCalldata);

require(ok2, "sell failed");

uint256 endBalance = IERC20(tokenOut).balanceOf(address(this));

require(endBalance >= startBalance + minProfit, "no profit");

}

真正的实现更加困难(处理原生 ETH、多个路由器、V3 池的回调)。将以上内容视为说明性的。

第 4 步:模拟每次尝试

提交之前,在分叉链上模拟交易:

anvil --fork-url $RPC_URL --fork-block-number latest

cast send --private-key $TEST_KEY $DISPATCHER \

"executeArb(bytes,bytes,address,uint256)" \

$BUY_CALLDATA $SELL_CALLDATA $WETH 1000000

如果模拟成功且利润 > min_profit,则您可以发送。跳过模拟是初学者机器人恢复的第一大原因。

第 5 步:提交

对于 Base,提交到公共内存池(2026 年大多数 L2 上还没有 PBS)。使用中等优先级费用登陆下一个区块:

js

const tx = await wallet.sendTransaction({

to: DISPATCHER,

data: dispatchCalldata,

gasLimit: 500000,

maxFeePerGas: ethers.parseUnits('0.0015', 'gwei'),

maxPriorityFeePerGas: ethers.parseUnits('0.0005', 'gwei')

});

const receipt = await tx.wait();

console.log('Status:', receipt.status, 'Gas used:', receipt.gasUsed);

如果 receipt.status === 1,你就成功了。查看 receipt.logs 以获取实际捕获的利润。

第 6 步:衡量发生了什么

您的前 20 次尝试主要会:

- 恢复(被另一个套利者抢先):50–70%

- 已落地但与模拟不同:记录最终回执,并说明状态、费用和排序差异

- 成功落地且盈利:10–25%

这很正常。该比率会随着您的调整而提高(更低的延迟、更好的信号过滤、更智能的调整)。

要记录的内容:

- 决策时观察到的传播

- 着陆时观察到的传播

- 预测利润与已实现利润

- 使用的Gas与估计的Gas

- 为什么每次恢复都会发生(Foundry 跟踪帮助)

第 7 步:拉紧环

100 次尝试后,您将看到以下模式:

- 传播到某个阈值之上更可靠

- 某些时段套利频率较高

- 特定竞争对手在某些窗口中比您更快

使用模式来过滤您提交的内容。提交更少、更高质量的尝试胜过喷洒。

常见的 First-Bot 错误

- 缺少批准:合同在第一次致电时恢复。在部署脚本中添加无限批准。

- 错误的池费用等级:数学表示利润,实际掉期表示损失,因为数学使用 5bp 池,但称为 30bp 池。

- 陈旧储备:读取区块 N 的储备,在区块 N+1 提交——状态漂移。重新阅读合同内部或使用基于回调的定价。

- 滑点上限太紧:原本会略有盈利的交易会恢复。根据实际实现与模拟进行校准。

- 代币小数位数:USDC 有 6 位,WETH 有 18 位。数学中相差 12 是一个常见的错误。

两池之后下一步是什么

一旦双池套利运行干净:

- 三池三角套利:USDC → WETH → DAI → USDC。

- 具有寻路功能的多重 DEX:动态选择使用 N 个池中的哪两个。

- JIT 流动性:围绕即将到来的掉期提供和拉动 LP。

- 跨链套利:需要桥接成本建模(高级)。

技能堆栈复合:池数学→呼叫数据→模拟→延迟→出价。二池原子是基础。

常问问题

我必须自己写智能合约吗?

为了学习,是的。对于生产,FRB Agent 在每个支持的链上发送经过验证的调度程序合同。在生产中使用内置插件;在 dev 中编写自己的代码来理解它们。

为什么大多数尝试都无利可图?

您正在与具有更低延迟、更好的信号过滤和预先批准的流动性的机器人竞争。初学者获得剩余的点差。没关系——还有一些剩菜值得捕捉。

我应该从多少资金开始进行套利?

2000-5000 美元。低于此水平,Gas对资本是敌对的。在此之上,您可以在调整后进行缩放。

这是策略三明治攻击吗?

不会。DEX 之间的双池套利不会从用户的互换中提取——它会均衡各个池之间的价格。这是协议积极的。

我可以在以太坊 L1 上运行它吗?

技术上是的,作为初学者在经济上是痛苦的。每次尝试 10-50 美元的 L1 Gas 会吞噬交易规模 <5 万美元的大部分价差。从 L2 开始。

相关阅读

这是一个工程教程。仅在测试网或纸质交易模式下运行后才能部署资金。不是财务建议。

相关文章

延伸阅读与工具

讨论

暂无笔记。添加第一条观察,或在以下平台与团队分享链接 X (@MCFRB).